Sustainability Reporting for Automotive Suppliers

Many manufacturers will soon be required to disclose their impacts on the environment. How will that impact their suppliers?

It seems as if every month there’s a new mandatory environmental, social, and governance (ESG) corporate disclosure. While the details on who needs to comply with these new rules and regulations vary for public or private companies, or based on different factors like location of operations and company size, ultimately each mandates that companies accurately and transparently disclose how their operations impact people and the planet. These rules and regulations will make it difficult for companies to hide behind empty sustainability goals and, ideally, lead to more credible pathways for environmental and social impact progress.

A few recent examples include:

California’s SB 253 and SB 261: Passed by California’s legislators in mid-September, SB 253 will require all private and public companies operating in California with an annual revenue exceeding $1 billion to publicly disclose their Scope 1 (direct operations) and Scope 2 (electricity use) greenhouse gas emissions by 2026. By 2027, these companies will be required to report emissions stemming from their value and supply chains, or Scope 3 emissions. Additionally, SB 261 will require U.S. companies with revenue of at least $500 million that do business in California to biennially publish climate risk reports in accordance with the Task Force on Climate-Related Financial Disclosures (TCFD). This framework requires companies to describe their corporate governance systems and disclose their greenhouse gas emissions, climate-related metrics and targets, and strategies for risk mitigation.

Corporate Sustainability Reporting Directive (CSRD): CSRD will apply to companies either based in the European Union or with significant operations there that meet at least two of the following criteria: have more than 250 employees, an annual turnover of more than €40 million, or total assets greater than €20 million. Companies will be legally required to report on the material social and environmental impacts, risks, and opportunities identified in their own operations and those of their upstream and downstream value chain – including disclosures on Scopes 1, 2, and 3 greenhouse gas emissions and transition risks.

U.S. Security and Exchange Commission (SEC)’s proposed climate-related disclosures: This proposed rule will require public companies to disclose certain climate-related information including greenhouse gas emissions, climate-related physical and transition risks and impacts, and oversight of these risks in alignment with the TCFD framework. Scope 3 supply emissions data is required for certain companies. The rule also requires limited assurance on companies’ first emissions data, moving to reasonable assurance over time. While the timing of this rule remains in flux, it is now anticipated to be finalized by the SEC in April 2024.

How Do These Mandatory Corporate Disclosures Impact Automotive Suppliers?

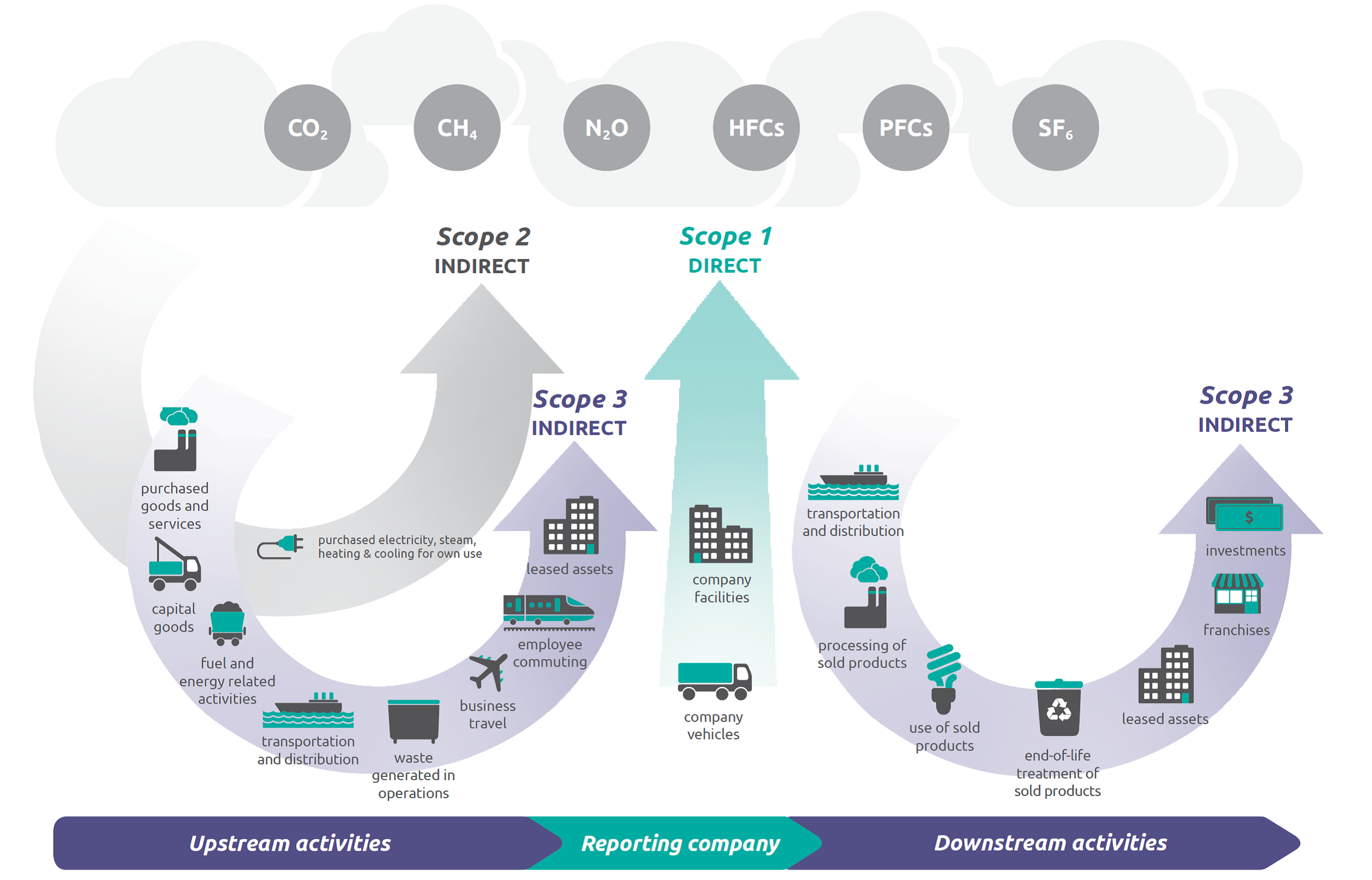

To understand how these corporate disclosures will impact automotive suppliers, it’s important to first understand Scope 3 emissions and the supply chain. Reporting on Scope 3 requires companies to account for the emissions sources that occur across their upstream and downstream supply chains: the network of suppliers that provide physical components and transport raw materials to product sites, as well as transportation suppliers for the final product (e.g., warehousing).

Consider this situation: A leading automotive manufacturer is required to disclose their Scope 3 emissions under California’s new SB 253 emissions disclosure law. To do so, the company will rely on each of its partners across their supply chain. Automotive suppliers will need to be able to provide their own emissions data to their manufacturing customer in order for their customer to satisfy the Scope 3 requirement of the law. In other words, if a supplier sells to another company that is required to comply with the law, it will need to account for the emissions produced during the production and transportation of that good for the customer.

Understanding Scope 1, 2, and 3 greenhouse gas emissions (credit GHG Protocol)

Additional Benefits of Sustainability Reporting for Automotive Suppliers

As automotive suppliers understand and disclose their impacts on the environment and human rights in order to support manufacturers, there is also an opportunity for them to enhance their own reputation by releasing annual public ESG reports. Understanding, managing, and disclosing these topics can have crucial internal and external benefits, including:

Enhanced reputation and trust: Transparent reporting can enhance reputation, increasing loyalty and strengthening trust from customers, employees, investors, and partners.

Engaged employees: Sustainability reporting instills a sense of responsibility. When employees are aware of their employer’s sustainability commitments and their individual role in creating change, they are reported to have greater job satisfaction.

Risk management: Reporting aids in identifying potential business risks and opportunities. Proactively addressing these issues mitigates risk and helps safeguard businesses from negative consequences.

Are you an automotive supplier ready to learn more about completing an emissions inventory or setting emissions reduction targets? Do you want to learn more about how that work ties into developing your own ESG reports? No matter your environmental or social impact stage, we’re here to help. Reach out to The Uplift Agency at hello@theupliftagency.com.

The Uplift Agency

Uplift builds strategies, programs, and communication campaigns that advance ESG in workplaces, supply chains and communities.

We know how to navigate the road ahead because we’ve already been down it – 90 percent of our team has led environmental or social programs in corporations or nonprofits. Because ESG is all we do, our services are more comprehensive and integrated than most firms.